Similar to depreciation, amortization is effectively the “spreading” of the initial cost of acquiring intangible assets over the corresponding useful life of the assets. The amortization of intangible assets is defined as the systematic process of allocating the cost of an intangible asset over its useful life. Per generally accepted rate of return ror meaning formula and examples accounting principles (GAAP), businesses amortize intangibles over time to help tie the cost of an asset to the revenues it generates in the same accounting period. To calculate the annual amortization expense for your patent, you need to divide the total cost to obtain the patent by the length of the amortization period.

Stay up to date on the latest accounting tips and training

In such a case the investment opportunity is essentially zero, so the owner should make the decision based on other, nonfinancial factors. At the end of the day a business should be able to assign an approximate worth to its patent portfolio. Is a question that can be very difficult to answer, and can result in multi-million-dollar litigation decisions, or patent applications being abandoned before they even issue. Considering the $100k purchase of intangibles each year, our hypothetical company’s ending balance expands from $890k to $1.25 million by the end of the ten-year forecast. Upon dividing the additional $100k in intangibles acquired by the 10-year assumption, we arrive at $10k in incremental amortization expense. The basis for doing so is based on the need to match the timing of the benefits along with the expenses under accrual accounting.

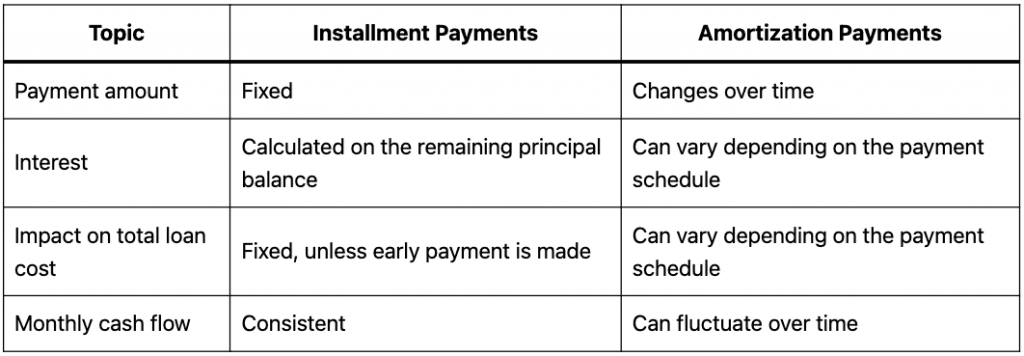

Amortization vs. Depreciation

Patent amortization is a nuanced topic that requires careful consideration of legal, financial, and strategic factors. It’s a tool that, when used wisely, can enhance the financial health of a company and support long-term innovation strategies. Understanding the intricacies of patent amortization is essential for inventors and businesses to maximize the value of their intellectual property. Impairment losses, if any, are also reflected on the income statement, impacting net income. Regular impairment testing ensures that the carrying amount of the patent does not exceed its recoverable amount, maintaining the integrity of the financial statements.

Purchase and sale of intangible assets

If this pattern cannot be reliably determined, a straight-line method is applied, which evenly distributes the cost over the useful life. From the inventor’s or company’s standpoint, effective patent amortization can be a tool for strategic financial planning. By carefully selecting the amortization method and timing, a company can manage its earnings and tax liabilities. The straight-line method is commonly used, where the patent’s cost is evenly spread over its useful life.

- If a patent does not supply worth, or supplies a decreased degree of worth, it is important to acknowledge the impairment and scale back or get rid of the carrying quantity of the asset.

- This method is particularly useful for patents that are integral to a company’s revenue stream.

- In this case, the DCF value is only barely above the cost of maintenance fees.

- An impairment test is conducted when there is an indication that the patent may be impaired, which means its carrying amount may not be recoverable.

- The significant non-cash investing activities are, however, disclosed in the footnotes under the caption “non-cash investing and financing activities”.

Patent Amortization: Everything You Need to Know

The amortization schedule would detail the monthly payments of $188.71, with the initial payments being mostly interest and gradually shifting towards the principal. This allows the inventor to see that, after the first year, they will have paid $2,264.52, but only $1,748.60 will have gone towards the principal balance, with the rest covering interest. Such insights are invaluable for planning and managing financial commitments related to patenting.

Impact on Financial Statements

A robust patent portfolio can demonstrate innovation and market potential to investors. Take the case of a small tech company with a groundbreaking software algorithm; by patenting it, they can increase their valuation and attract venture capital. Explore the intricacies of patent accounting in financial reports and tax filings, ensuring compliance and accurate valuation in your business practices. Be aware that the research and design (R&D) prices required to develop the thought being patented cannot be included as part of the capitalized price of a patent. The concept behind this remedy is that R&D is inherently risky and without assurance of future gain, so it shouldn’t be thought of an asset. An equal debit to the credit score made within the final step needs to be made to the amortization expense account (in each instance).

GAAP allows only patents acquired from third parties to be recorded on your balance sheet and amortized. Debit the patent’s total cost to the patent account in a journal entry in your accounting records when you acquire the patent. The deciding factor on whether a line item gets capitalized as an asset or immediately expensed as incurred is the useful life of the asset, which refers to the estimated timing of the asset’s benefits. Under the straight-line method, an intangible asset is amortized until its residual value reaches zero, which tends to be the most frequently used approach in practice. Therefore, public companies must adhere to the matching principle in accounting by recording the entire expense on the income statement. For startups and small businesses, patents can be pivotal in attracting investment.

Amortization of intangibles (or amortization for short) appears on a company’s profit and loss statement under the expenses category. This figure is also recorded on corporate balance sheets under the non-current assets section. Tangible assets are expensed using depreciation, and intangible assets are expensed through amortization.

So to find an amortization expense, simply divide the asset’s value by its lifespan. The receipt of a cash dividend of $1,200 may be classified as either operating or investing cash inflow if financial statements are prepared in accordance with IFRSs. However, if GAAPs are to be followed, the cash received for dividends should be classified as operating cash inflow. During the year, it sold an old plant asset for $6,400 and purchased a tract of land for $1,500. The plant was purchased several years ago for $10,000 and was being depreciated using the straight-line method. The accumulated depreciation on the plant at the time of its sale was $4,000.

Failure to pay these fees can result in the patent lapsing, thereby losing its protective benefits. These ongoing costs must be factored into the long-term financial planning of a company, as they represent a recurring expense that can impact cash flow. Properly accounting for maintenance fees is essential for maintaining the value of the patent portfolio.

This method not only aids in tax savings but also in reflecting the true value of the intellectual property on the company’s balance sheet. By spreading out the expense, businesses can manage their cash flow more effectively and make more accurate financial projections. Amortization schedules serve as a critical tool for inventors and businesses to manage the financial aspects of patent portfolios. These schedules provide a systematic plan for paying off an obligation, such as a patent loan, over time.